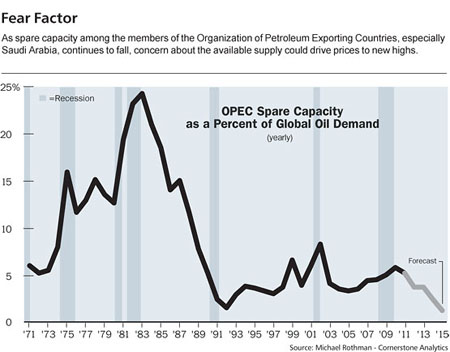

"As oil producers' spare capacity declines to worrisome levels, prices could reach new records."

The U.S. economy is never completely ready for higher oil prices, which is one reason they take a nasty economic toll when they arrive. But readiness can be enhanced by awareness of the likely outlook for petroleum prices—and the outlook today is relatively grim, although probably not disastrous.

Despite the recent 20% decline from April highs, new highs on crude, heating oil, diesel fuel, jet fuel and gasoline seem likely over the next 12 months. Following some further easing over the summer, the second leg of the long-term bull market in petroleum—the first occurred in 2007–2008—probably will begin this fall.

As oil producers' spare capacity gradually declines to worrisome levels, the average monthly price could reach a record $150/ barrel by next spring, with spikes to $165 or $170. With this, $4.50-a-gallon gasoline will become the norm.

The continued short-term easing of oil prices should benefit the economy over the summer, only to exact a much larger payback later. The projected oil shock of spring 2012 will hurt economic expansion, but not kill it, pruning about 1.5 percentage points from quarterly growth in real gross domestic product.

While painful, this forecast isn't quite as extreme as it might appear. Short-lived price spikes and troughs make for frenzied headlines in newspapers and on the Internet as well as for hysterical talking heads on radio and TV, but what matters for the economy are average prices over at least a few months. Barron's estimates that the effective price of crude was about $110 in this year's second quarter, which just ended. A projected increase to $150 by the second quarter of next year assumes a rise of $40. Oil is likely to stay at $150 for several months, before the promise of greater supply brings gradual easing.

Source: Barron's, Gene Epstein

No comments:

Post a Comment